24 Jun How to Finance Your Second Investment Property in NZ: Using Equity, Rental Income & Smarter Lending Strategies

How to Use Home Equity to Buy a Second Property in NZ: Smart Ways to Buy an Investment Property

For many homeowners in NZ, one of the most effective ways to grow wealth is by using home equity to buy a second property rather than saving an entirely new deposit from scratch. As the value of your property increases and your mortgage reduces over time, the equity in your home becomes a valuable financial resource that may be used to purchase an investment property, a holiday home or another property to expand your investment portfolio. Whether you are looking to buy a second home, start investing in property or purchase rental properties that generate rental income, understanding how equity works is the first step towards making informed borrowing decisions. Knowing how much equity you can use, the minimum equity requirements and how lenders assess your borrowing capacity can help you plan your next property purchase with greater confidence while adapting to changing interest rates and the New Zealand property market.

Many property investors use the equity in their existing property as a deposit for a new investment property, allowing them to leverage their existing assets rather than relying solely on cash savings. The right finance structure can make a significant difference to borrowing flexibility, long-term cash flow and future investment opportunities. Whether you are looking to build equity, buy a house for rental income or expand beyond one property, understanding how to use home equity strategically can help you move forward with confidence. If you are considering using your equity to invest in another property, speak with the team at Global Pacific Capital to explore finance solutions tailored to your investment goals and discover smarter ways to grow your property portfolio in New Zealand.

How much equity do I need to buy a second property and start property investment?

What is equity in your existing property and how is it calculated in NZ?

Equity is one of the most valuable financial assets available to homeowners looking to expand into property investment in NZ. Simply put, equity is the difference between the current market value of your property and the amount still owing on your mortgage. As your home loan balance reduces and the value of your home increases over time, the amount of equity available generally grows. For example, if your existing home is worth $1,000,000 and your remaining mortgage is $500,000, your equity in your existing property is $500,000. This equity can often be used to help fund another property purchase without needing to save a full cash deposit.

Many property investors use the equity in their current home to buy a second property or purchase an investment property that generates rental income and builds long-term wealth. Before borrowing, lenders usually require an updated valuation to determine the current property value and calculate how much equity you can use. Investors researching property investment loans in New Zealand should also understand that borrowing capacity is influenced by income, existing debt, interest rates and the overall strength of the New Zealand property market, not simply the amount of equity available.

How much of the value of your property can you use as home equity to buy a second?

The amount of home equity you can use depends on several factors, including the value of your property, your remaining mortgage balance and your lender’s borrowing policies. While many homeowners assume they can access all of their available equity, lenders generally require a portion of the property’s value to remain untouched as a safety buffer. This means the equity you can use is often less than the total equity shown on paper. Borrowing limits may also vary depending on whether you intend to buy a second property, purchase rental properties, invest in another property or acquire a holiday home. Understanding how leveraging home equity works is an important part of building a successful investment portfolio.

Lenders also consider your ability to service additional borrowing before approving finance for a second property in New Zealand. Income, existing financial commitments, rental income projections and current interest rates all contribute to the assessment. Investors should also consider future cash flow rather than focusing only on the amount of equity available today. Using your equity wisely can provide greater flexibility for purchasing a new investment property while maintaining enough financial capacity to manage unexpected expenses and changing market conditions over the long term.

What is the minimum equity or deposit lenders expect for investment properties?

Minimum equity requirements for investment properties in NZ can vary depending on the lender, the type of property being purchased and current lending policies. In many situations, lenders expect borrowers to contribute a larger deposit when purchasing an investment property than they would for an owner-occupied home. Rather than saving cash separately, many investors choose to use some of the equity in their existing property as a deposit, allowing them to leverage their current assets to purchase another property. The required amount of equity will often depend on the property’s value, the strength of the borrower’s financial position and the overall lending risk.

Lending policies can also change over time as economic conditions, interest rates and regulatory requirements evolve. Investors planning to build a property portfolio should carefully review minimum equity requirements before making a property purchase, particularly if buying an existing property or a new build. Maintaining sufficient equity after settlement can also provide greater flexibility for future borrowing, refinancing or expanding into additional investment properties. Understanding these lending requirements early helps investors make more informed decisions and develop a sustainable long-term property investment strategy.

Can I use equity to buy an investment property and how does borrowing work?

How do lenders assess equity to buy and lend against my current home?

Lenders assess several factors before approving the use of home equity to buy an investment property in NZ. The first step is determining the current market value of your property, usually through a registered valuation or an approved valuation model. They then compare this figure with the outstanding balance on your mortgage to calculate the available equity. While equity is the difference between what your current home is worth and what you still owe, not all of that equity is generally available for borrowing. Lenders also assess income, existing financial commitments, credit history and the ability to service additional debt before approving finance for a second property or expanding an investment portfolio.

Once the amount of usable equity has been established, lenders evaluate whether the proposed borrowing remains within acceptable lending limits and minimum equity requirements. The assessment also considers the purpose of the loan, whether you intend to buy a second home, purchase rental properties or acquire another property as part of a long-term property investment strategy. Investors exploring property investment FAQs can gain a better understanding of how borrowing structures, lending policies and equity work together when financing investment properties in New Zealand. Understanding these factors before applying can improve borrowing confidence and reduce delays during the approval process.

How does borrowing with equity affect my mortgage and interest rates?

Using equity in your home to purchase another property increases the overall amount borrowed, which may affect mortgage repayments, loan structure and long-term cash flow. Depending on the finance arrangement, the additional borrowing may be added to an existing home loan or structured as a separate lending facility secured against your current property. Borrowers should consider how changing interest rates could influence monthly repayments, particularly if purchasing investment properties that rely on rental income to support borrowing costs. Planning for future interest rate movements is an important part of responsible property investment in New Zealand.

Borrowing against home equity can also create opportunities to build an investment portfolio more quickly without selling your current home or waiting years to accumulate another cash deposit. Many investors review fixed and floating mortgage options, loan terms and repayment flexibility before using equity to invest. Maintaining sufficient financial capacity after settlement is equally important, as unexpected expenses or temporary changes in rental income can affect cash flow. A carefully structured lending arrangement helps support long-term property investment while reducing unnecessary financial pressure as market conditions evolve.

Can I use equity in your home to purchase a holiday home or rental properties?

Home equity can often be used to help finance a wide range of property purchases in NZ, including rental properties, a holiday home or a second property intended for long-term investment. Many homeowners choose to leverage their equity instead of saving an entirely new deposit, allowing them to expand their property holdings while continuing to benefit from the growth in their existing home. Whether purchasing a new investment property, buying an existing property or investing in another property, lenders will assess both the available equity and the borrower’s ability to manage the additional borrowing before approving finance.

The suitability of using equity depends on personal financial circumstances, investment goals and the expected performance of the new property. Rental properties may generate ongoing rental income that contributes towards mortgage repayments, while a holiday home may offer different financial outcomes depending on how it is used. Investors should also consider maintenance costs, insurance, ongoing borrowing commitments and long-term property value growth before proceeding. A balanced investment strategy focuses not only on acquiring another property but also on ensuring the overall property portfolio remains financially sustainable through changing market conditions.

What mortgage and home loan options are best for buying a second property?

Should I refinance my home loan to access equity to buy a second property?

Refinancing an existing home loan is one of the most common ways homeowners in NZ access equity to buy a second property. As the value of your property increases and your mortgage balance reduces, refinancing may allow you to unlock a portion of your home equity without selling your current home. The additional borrowing can often be used as a deposit for investment properties, helping property investors expand their portfolio while preserving available cash. Whether you are planning to buy a second home, purchase rental properties or start investing in property, refinancing can provide greater flexibility than saving a new deposit over several years.

Before refinancing, it is important to understand how the new borrowing will affect your mortgage repayments, loan term and overall financial position. Lenders assess the market value of your property, your income, existing commitments and the amount of equity available before approving additional lending. Homeowners comparing different borrowing strategies often review mortgage restructuring options to determine whether refinancing provides a more effective way to access equity while supporting long-term property investment goals. A well-structured refinance can improve borrowing flexibility while helping investors prepare for future property purchases.

What property loans or mortgage types suit investment properties in NZ?

Choosing the right home loan or mortgage structure is an important part of building a successful property investment portfolio in New Zealand. Different property loans are designed to suit different investment objectives, whether purchasing a single rental property, buying an additional property or expanding into multiple investment properties over time. Some borrowers prefer fixed interest rates to provide repayment certainty, while others choose floating rates for greater flexibility if they intend to reduce debt or refinance in the near future. The most suitable loan structure often depends on borrowing capacity, expected rental income, long-term investment goals and how quickly the investor plans to grow their portfolio.

Investors should also consider how different mortgage structures affect cash flow, equity growth and future borrowing opportunities. Splitting loans across multiple facilities or separating owner-occupied lending from investment borrowing may offer greater financial flexibility as property values change. Understanding how loan terms, repayment options and interest rates influence long-term costs can help investors make better financial decisions throughout their investment journey. Selecting the right finance structure at the beginning often creates greater opportunities to purchase additional properties while maintaining a sustainable level of borrowing.

When is it better to get a home loan specialist for investing in property?

Purchasing a second property or using home equity to invest can become more complex than arranging finance for a first home. As borrowing requirements, lending policies and property investment strategies become more detailed, many investors seek guidance from a home loan specialist to better understand available finance options. This is particularly relevant when using equity in your existing property, purchasing multiple investment properties or exploring lending solutions outside traditional bank products. A specialist can help explain different borrowing structures, minimum equity requirements and the financial implications of expanding a property portfolio.

Professional guidance can also be valuable when income sources are more complex or when borrowers are considering buying an existing property, a new investment property or a holiday home. Every lender has different lending criteria, and finance structures that work for one borrower may not suit another. Understanding how borrowing capacity, equity, rental income and long-term investment plans interact allows property investors to make informed decisions before committing to another mortgage. Careful planning at this stage can support stronger financial outcomes and create a more sustainable foundation for future property investment growth.

How will rental income and existing properties affect my ability to buy a second property?

How do lenders calculate rental income from existing properties when assessing borrowing?

Rental income can play an important role when lenders assess borrowing capacity for a second property in NZ, although it is not always counted at its full value. Most lenders consider the income generated from existing properties alongside employment income and other financial commitments to determine whether a borrower can comfortably manage additional mortgage repayments. They will also assess expenses associated with the property, including rates, insurance, maintenance and existing home loan obligations. The overall goal is to establish whether the rental properties contribute positively to cash flow and support long-term borrowing without placing unnecessary financial pressure on the borrower.

Lenders also consider the stability of rental income and the quality of the investment properties within the portfolio. Well-maintained properties with consistent tenant demand may strengthen a borrowing application, while extended vacancy periods or high operating costs may reduce borrowing capacity. Investors looking to purchase another property often review home loan options for investment properties to better understand how rental income, equity and lending criteria work together when financing additional property purchases. Careful planning before applying for finance can improve the likelihood of approval and create greater flexibility for future investment.

Can rental income cover the mortgage on a new investment property?

Rental income can contribute significantly towards mortgage repayments on a new investment property, but it should not be viewed as the only source of funding. Rental demand, vacancy periods, maintenance costs and changing interest rates all influence how much of the mortgage is covered by rental income over time. Investors should prepare realistic cash flow forecasts that account for periods when a property may be vacant or require unexpected repairs. Building sufficient financial reserves alongside rental income provides greater security and helps maintain a sustainable property investment strategy through changing market conditions.

Successful property investors generally focus on long-term financial performance rather than relying solely on immediate rental returns. In some cases, a property may initially require additional financial support while equity grows and rental income increases over time. As the property value rises and mortgage balances reduce, overall equity within the investment portfolio may strengthen, creating opportunities to leverage equity for future property purchases. Careful financial planning allows investors to balance rental income with borrowing commitments while continuing to build wealth through property investment in New Zealand.

How does owning multiple investment properties affect my investment portfolio and lend capacity?

Owning multiple investment properties can strengthen an investment portfolio by creating additional rental income streams and increasing long-term equity growth. As each property increases in value and mortgages reduce over time, investors may build greater borrowing capacity through accumulated equity. Diversifying across different property types or locations can also reduce risk by spreading exposure across different areas of the New Zealand property market. A well-managed portfolio often provides greater flexibility for future borrowing, refinancing and purchasing another property as investment opportunities arise.

At the same time, lenders assess the combined financial position of the borrower rather than considering each property in isolation. Existing mortgages, rental income, operating expenses, interest rates and available equity all influence future lending decisions. Expanding a property portfolio requires careful management of debt levels and cash flow to ensure borrowing remains sustainable over the long term. Investors who regularly review their financial position and maintain healthy equity across existing properties are generally better placed to continue growing their portfolio while adapting to changing lending conditions and market cycles.

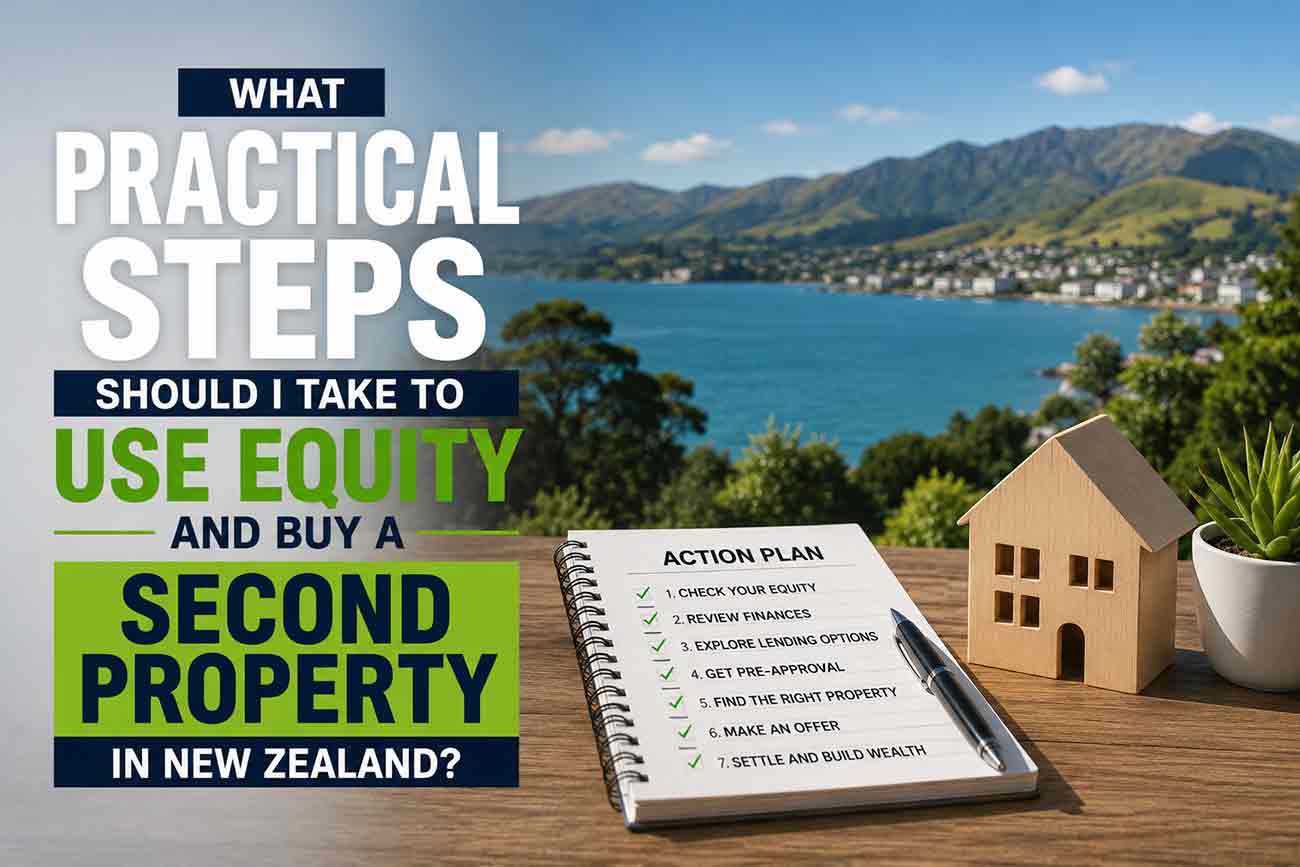

What practical steps should I take to use equity and buy a second property in New Zealand?

How do I determine the market value of your property and amount of equity available?

The first step in using home equity to buy a second property is establishing the current market value of your property. Lenders generally rely on a professional valuation or an approved valuation model to determine what your existing home is worth in the current NZ property market. Once the market value of your property has been confirmed, the remaining mortgage balance is deducted to calculate the available equity. Equity is the difference between what your property is worth and what you still owe, although only a portion of that equity may be available for borrowing depending on lending policies and minimum equity requirements.

After calculating the amount of equity available, lenders assess your overall financial position before approving additional borrowing. Income, existing debts, interest rates and the purpose of the new property purchase all influence how much equity you can use. Investors looking to understand the practical process of using equity often benefit from reading about buying property in New Zealand, including how valuations, borrowing capacity and lending criteria work together before purchasing an investment property. Taking the time to assess your financial position before searching for another property can help create a smoother purchasing process.

What documentation and deposit will lenders require to purchase an investment property?

Applying for finance to purchase an investment property requires lenders to review a range of financial documents alongside the proposed property purchase. Borrowers are commonly asked to provide proof of income, identification, bank statements, details of existing mortgages and evidence relating to current assets and liabilities. If using equity in your existing property as a deposit, lenders may also require an updated valuation confirming the current home value and available equity. Preparing this documentation early can speed up the approval process and reduce delays once a suitable property has been found.

Deposit requirements can vary depending on the lender, the property type and the borrower’s overall financial position. Some investors use cash savings, while others choose to use some of the equity in their existing home as a deposit for a new investment property. Lenders also assess the expected rental income, overall borrowing levels and the long-term affordability of the loan before granting approval. Understanding these requirements before beginning your property search allows investors to approach the market with greater confidence and realistic expectations.

What are the tax, property manager and buy-and-sell considerations when investing in property?

Successful property investment involves more than securing finance and purchasing another property. Investors should also consider ongoing tax obligations, property management responsibilities and long-term ownership objectives before building an investment portfolio. Rental properties require regular maintenance, insurance, rates and financial record-keeping, while changes in tax legislation can influence overall investment returns. Some investors choose to self-manage their properties, while others engage a property manager to oversee tenant selection, inspections and day-to-day administration. The right approach often depends on the size of the portfolio, available time and investment goals.

Planning an eventual buy-and-sell strategy is equally important when purchasing investment properties. Investors should consider whether they intend to hold the property for long-term capital growth, generate consistent rental income or sell the property when market conditions become favourable. Factors such as property value growth, equity accumulation, interest rates and broader New Zealand property market trends can all influence future decisions. A well-planned strategy helps investors make informed choices throughout the ownership cycle while supporting sustainable long-term property investment.

Conclusion

Using home equity to buy a second property can be one of the most effective ways to grow long-term wealth through property investment in NZ. By understanding how equity in your home is calculated, how lenders assess borrowing, and how rental income, deposits and mortgage structures work together, homeowners can make more informed decisions before purchasing another property. Whether your goal is to buy an investment property, expand an investment portfolio, purchase rental properties or invest in another property, careful planning is essential. Reviewing the market value of your property, understanding the amount of equity available and choosing the right property type all contribute to a stronger financial position while reducing unnecessary borrowing risk. As New Zealand’s property market continues to evolve, a disciplined approach to leveraging home equity can create opportunities to build equity and increase long-term property value.

Every property investor has different financial objectives, and the right lending strategy will depend on your current home, existing properties, borrowing capacity and future investment plans. Whether you are considering using your equity as a deposit, refinancing your home loan or purchasing a new investment property, having a well-structured finance solution can make the process significantly easier. For tailored guidance on using home equity to buy a second property, investment property finance and flexible lending solutions, speak with the experienced team at Global Pacific Capital. With practical expertise across property investment, home loans and financing strategies, they can help you structure your borrowing with confidence and support your long-term property goals in New Zealand.